United States

United States United Kingdom

United Kingdom As cryptocurrencies are facing issues of scalability, Visa and Mastercard has disadvantages as well. The issue with Visa, Mastercard, Eurocard, and even AMEX is that the merchant has practically no control over the transaction. Credit card companies process the transaction and decide whether the merchant will receive funds or not. Modern Finance (MF) Chain is working to create a cryptocurrency ecosystem that resolves the issues associated with traditional credit card transactions, accelerate crypto adoption, and provide a ready path for cryptocurrencies to integrate with commerce.

As cryptocurrencies are facing issues of scalability, Visa and Mastercard has disadvantages as well. The issue with Visa, Mastercard, Eurocard, and even AMEX is that the merchant has practically no control over the transaction. Credit card companies process the transaction and decide whether the merchant will receive funds or not. Modern Finance (MF) Chain is working to create a cryptocurrency ecosystem that resolves the issues associated with traditional credit card transactions, accelerate crypto adoption, and provide a ready path for cryptocurrencies to integrate with commerce.

Cryptocurrencies have achieved exponential growth in the past two years. Correspondingly, crypto investors have amassed massive wealth. Despite the extraordinary growth, mass adoption of cryptocurrencies is still a dream. Most of the blockchain projects innovate within their ecosystem and remain isolated. Modern Finance Chain aims to break down these common barriers that prevent mass adoption of cryptocurrencies and blockchain technology in general.

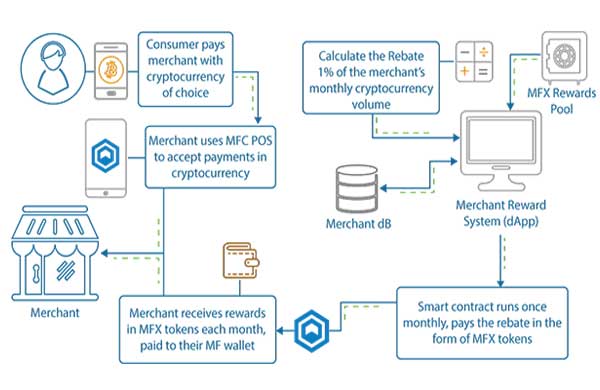

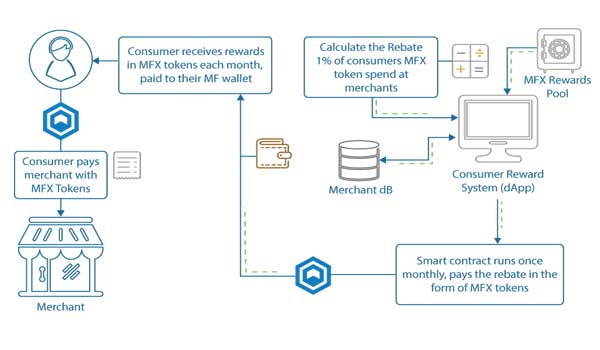

MF is building a cryptocurrency payment system that rewards both consumers as well as the merchant. The innovative merchant rewards program and zero-fee model make it the most cost-effective cryptocurrency payment system.

MF’s roadmap includes the development and deployment of MF Mainnet, an independent public blockchain that uses a BFT/POS consensus model and a unique masternode incentivization protocol. Furthermore, MF Mainnet will allow for the development of enterprise level private blockchains, multi-blockchain integration, atomic swap cross-chain transactions, and a verified digital identity system. With a BFT/POS hybrid consensus method, MF Mainnet will achieve consensus with minimal energy consumption and in an eco-friendly manner.

MF Mainnet is built as a currency agnostic system that functions either with or without a tokenized economy. However, MF Mainnet also offers the flexibility of transacting with a variety of cryptocurrencies, such as BTC, ETH, etc., thus freeing ICOs from the limitations they encounter throughout the process of their initial launch.

The global mobile payment market is projected to exceed $1 trillion by the year 2019. The total global non-cash transactions were $522 billion in 2017, and this number is likely to reach $725 billion over the next two years. Mobile payments will continue to rise at a CAGR of approximately 22% as supported by the increased proliferation of mobile devices and mobile payment applications.

As the number of alternative payment types has grown, traditional means of online payment, like credit cards, are on the downgrade as they are fighting with competition that offers higher user-friendliness, more security, and lower costs.23 As Koley reports, even though the virtual duopoly of Visa and MasterCard is still experiencing healthy growth rates (9.5% and 9.6%, respectively) and remains the preferred method for (offline) point-of-sale (POS) transactions, firms like JCB and UnionPay outperform them by far (growing 20.7% and 44.8%, respectively).

The main issue with incorporating cryptocurrency as a method for merchant-consumer payments is volatility. Additional concerns are centered on cryptocurrency transactions fees and transaction processing time. The merchant reward system adopted by Modern Finance Chain resolves these existing issues.

Merchant Reward System

Merchants are rewarded a 1% rebate of their total cryptocurrency volume in the form of MFX Tokens. MFX Tokens are valued based on $1 per token or their current exchange rate, whichever is greater, at the time of settlement. Each month merchant statement is evaluated from the previous month’s processing. Statement evaluation closes on the last day of each month. Rewards payments are settled on the 7th day of each month.

MFX reward pool

The MF Chain reward pool consists of 75M MFX Tokens and the rebate programs will continue for an additional 5 or more years. Additional reward pools will be added to the program as partnerships with other projects develop. This will allow merchants and consumers to receive multiple reward tokens for a single transaction. Partnerships will likely extend the program in perpetuity.

With the launch of MF Mainnet, the MFF token will take the place of the MFX token within the rewards programs, allowing merchants and consumers to receive transaction fuel for MFM.

The decentralized part of the MF Chain business logic is written in the form of smart contracts. We’re using the Open Zeppelin library for writing secure smart contracts on Ethereum in Solidity programming language. The token smart contract is a standard ERC20 implementation with ERC223 additions that secure the token holders from accidental token loss if they are sent to an ineligible contract. The MFX token is compatible with any existing ERC20 wallet. Consumers will have the ability to use their existing wallets to store tokens and make payments.

Commencing crypto transaction

The list of supported cryptocurrencies initially includes but is not limited to:

BTC

ETH

LTC

MFX

Merchants are in full control of their cryptocurrency wallets because they do not share, import, or upload the private keys to the MF Chain platform. Merchants can download a free mobile app that will transform any mobile device to a fully functional Point of Sale system with all MF Chain features.

Once authorized the app is ready to create orders and accept cryptocurrency to the merchant’s wallets that are configured in their accounts. Both Android and iOS platforms are supported.

The user flow is as simple as with credit card point of sale (POS) terminals: the order amount is entered, user selects the preferred cryptocurrency, and receives the QR code to complete the payment using the mobile wallet app on their smartphone. After the payment is completed the merchant can view the transaction confirmation status. The system can be configured to rely on any number of consensus node confirmations through merchant settings to declare a payment success. Merchants are afforded the same flexibility with the MF Chain Mobile POS Client App.

MF Chain will integrate with merchants in 2018 by partnering with payment processors that are already doing business with a minimum of 10,000 merchants. Payment processors will be engaged with an incentivized partnership agreement that brings an exciting new service to their merchant product offerings.

Support for external projects

Projects approved for the Modern Finance Chain Innovation Incubator are supported by MF Chain on multiple strategic fronts: Access to the pre-built and audited smart contract library, an ICO launch platform that is multi-currency capable and development & marketing support. MF Chain will directly benefit from equity ownership in these projects.

Modern Finance Chain (MF Chain) plans to raise between 2,500 and 33,000 ETH Tokens during the Pre-ICO and ICO. All ICO transactions are completed via smart contract transfer.

MF Chain ICO details

Private Offer: April 5 – May 5

Presale: May 6 – May 25

ICO: May 26 – June 25

Soft Cap: 2,500 ETH (with built in smart contract refund feature if not obtained)

Hard Cap: 33,000 ETH

The total number of MFX tokens is capped at 521,000,000. 1 Ether = 8,500 MFX tokens.

ICO Token Price: 1 Ether = 8,500 MFX Tokens

33,000 Ether Total ICO Hard Cap

Minimum Contribution – 0.1 Ether

Maximum Contribution – 200 Ether

Presale Token Price: 1 Ether = 10,150 MFX Tokens

5000 ETH Hard Cap

Minimum Contribution – 5.0 Ether

Maximum Contribution – 200 Ether

=>10 ETH: 10% Bonus

=>25 ETH: 15% Bonus

=>100 ETH: 20% Bonus

Tokens allocation

Presale & ICO – 57% (301M)

Airdrop & Incentive Programs – 1% (5M)

Devs & Advisors – 8% (40M)

Merchant Incentive Program – 15% (75M)

Locked tokens to support development & marketing – 19% (100M)